We introduce XBRL2Vec, a financial data engine designed to vectorize corporate filings into structured representations for next-generation capital allocation systems. Unlike traditional investment frameworks that rely on backward-looking price series or simplistic ratio-based metrics, XBRL2Vec extracts and embeds GAAP-tagged fundamentals, narrative disclosures, and risk language into multi-dimensional vectors. The result is a flexible, machine-readable representation of a firm’s financial and strategic position—enabling downstream AI systems to allocate capital in contextually grounded, economically meaningful ways.

1. Introduction

Financial markets are inundated with raw disclosure data—yet most algorithmic trading systems fail to incorporate it meaningfully. Traditional quantitative systems emphasize historical prices, volume, and derived indicators, leaving narrative content and detailed financial fundamentals underutilized.

XBRL2Vec addresses this gap by converting raw corporate filings (e.g., 10-K, 10-Q) into rich numerical representations. By marrying fundamental analysis with natural language processing (NLP) and representation learning, XBRL2Vec makes it possible for AI agents to reason over qualitative disclosures and quantitative performance with the same precision.

2. System Overview

2.1 Architecture

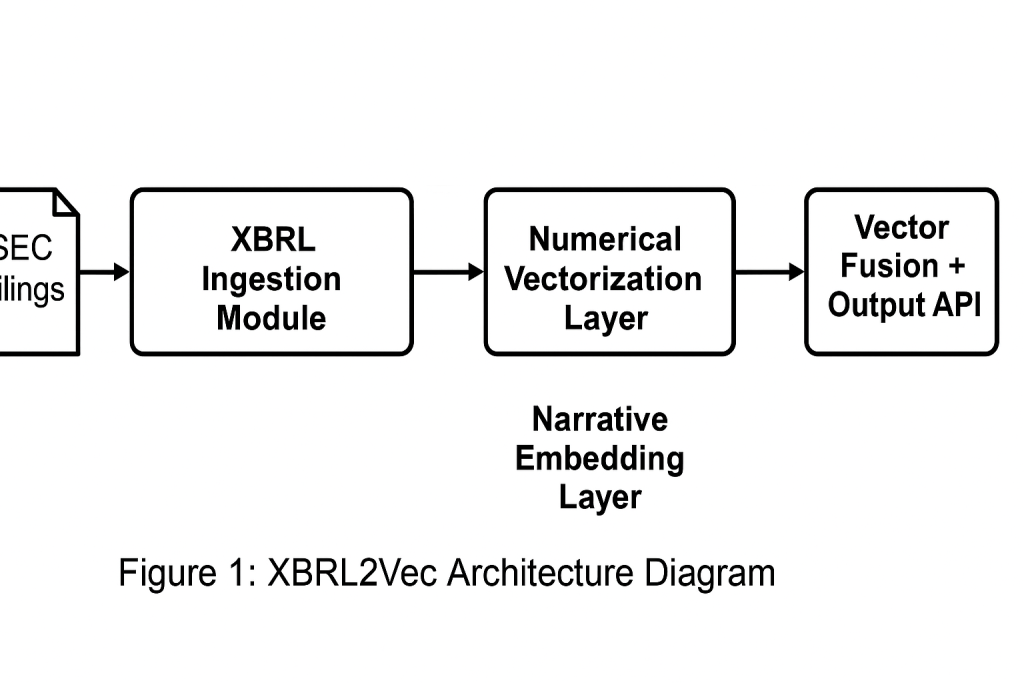

The XBRL2Vec pipeline consists of four major components:

XBRL Ingestion Module

Parses structured SEC filings using US GAAP taxonomy

Handles footnotes, tables, nested hierarchies

Numerical Vectorization Layer

Standardizes financial statement elements (revenue, margins, assets, etc.)

Extracts MD&A, risk factors, legal contingencies, etc.

Uses transformer-based models (e.g., FinBERT, LegalBERT) to generate embeddings

Vector Fusion + Output API

Combines numerical and narrative embeddings

Outputs composite firm vectors for downstream modeling

Figure 1: XBRL2Vec Architecture Diagram (Include a block diagram showing ingestion → vectorization → fusion → API output)

3. Methods

3.1 Numerical Processing

We convert GAAP-tagged elements into structured tensors by:

Mapping raw disclosures into a fixed schema

Time-normalizing (TTM, quarterly change)

Scaling (industry-relative or market percentile)

3.2 Narrative Embedding

Text sections are split and embedded using:

Pretrained financial/legal transformers

Topic modeling (optional) for dimensional reduction

Sentence-level embeddings pooled into document vectors

Figure 2: Example Embedding: Risk Disclosure → Vector Space

4. Use Cases

Earnings Quality Forecasting Predict misstatements, restatements, or volatility based on narrative risk language + earnings dynamics

Systemic Risk Assessment Vector clustering to detect sector-wide exposure patterns from risk factors

Capital Allocation Layer (AI-Ready) Use firm vectors as input to reinforcement learning agents or allocation optimizers

5. Results (Prototype Stage)

Preliminary tests on ~1,000 S&P 500 filings show that narrative embeddings:

Improve earnings prediction accuracy vs. numerical-only baselines

Cluster meaningfully across sectors and business models

Enable semantic comparison of companies independent of ticker/price

Figure 3: UMAP projection of firm vectors showing sectoral separation

6. Future Work

Full EDGAR stream parsing and real-time inference pipeline

Integration with TradingLogic.ai execution engine

Plug-and-play compatibility with capital allocation models (RL agents, optimization systems)

7. Conclusion

XBRL2Vec represents a foundational shift in financial modeling—from signals to structured intelligence. By embedding both the numbers and the narratives, it allows machines to operate with a richer, more human-like context—bridging the gap between data and reasoned capital allocation.